- Because the market already exists. Regulation is catching up. Infrastructure has not.

- Because the EU has moved crypto into a unified CASP/MiCA regime, while the US has established its first federal framework for payment stablecoins.

- Because regulated market access is pulling digital assets deeper into institutional finance, while the infrastructure connecting them to real commerce remains largely unbuilt.

- Because this creates a limited window. The first company to validate compliant rails can establish the market position before banks, payment giants, and major fintechs move in.

- Because this round funds the first commercial version of Nostro before the banking layer and institutional expansion.

- Because €2M removes the biggest early-stage risks: technology, regulation, and commercial validation.

- Because the next round begins with working regulated infrastructure, real customers, and proven demand instead of assumptions.

- Because our financial model remains unchanged. Only the execution sequence changed. We prove the rails first, then scale the banking layer.

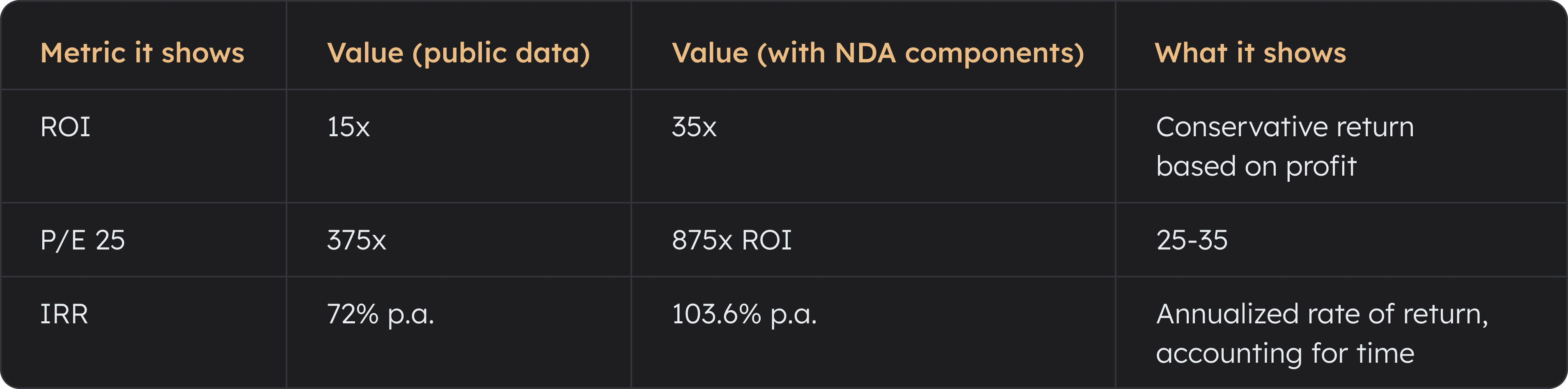

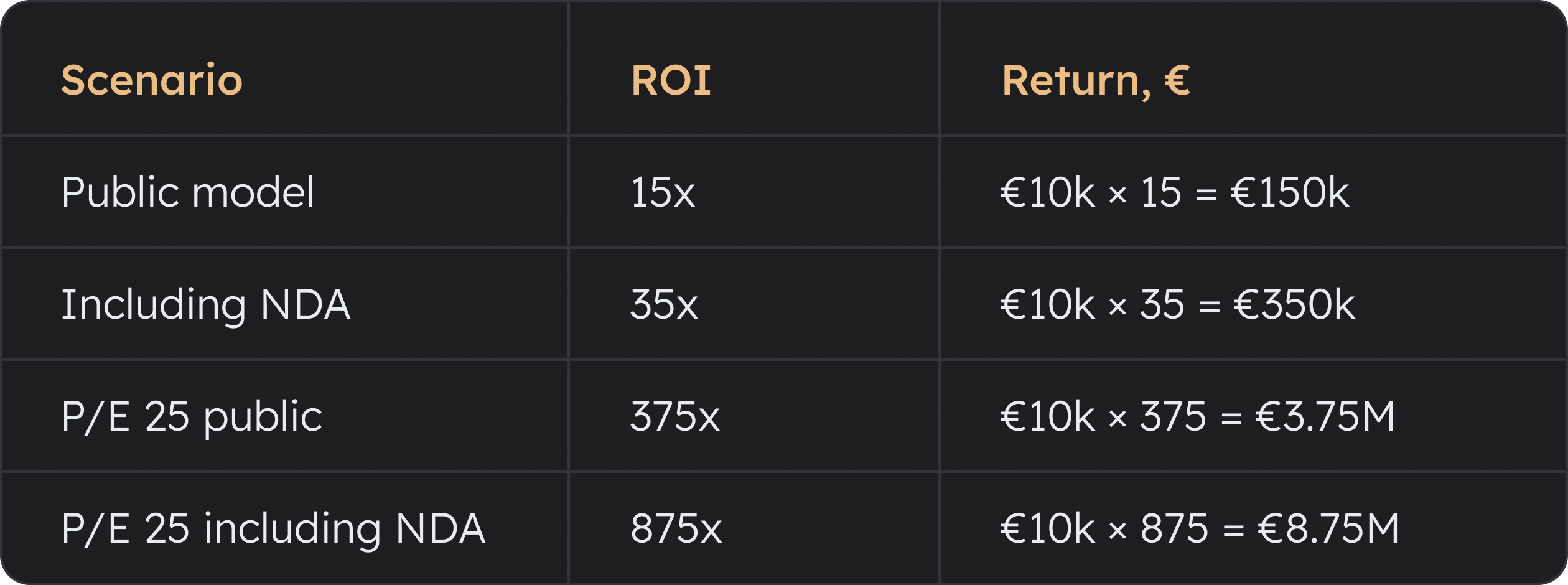

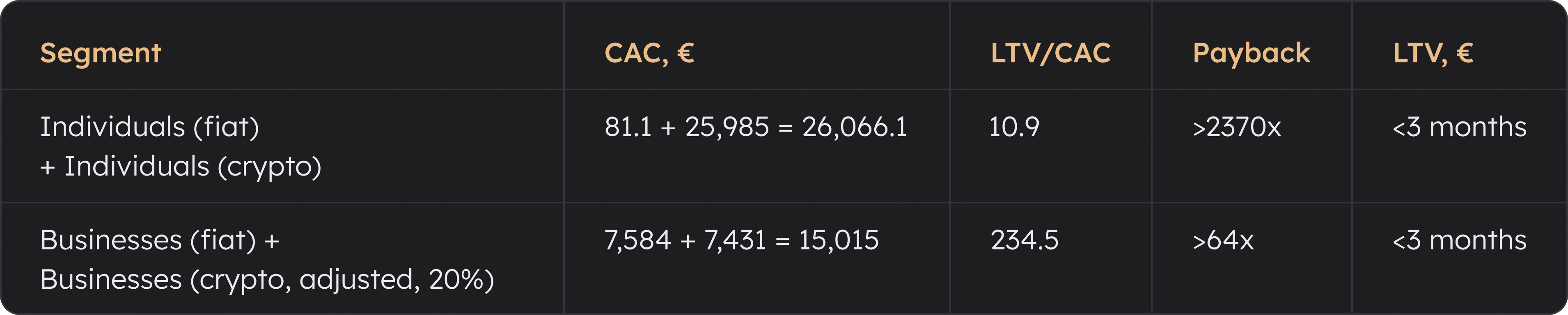

- Because our long-term model assumes capturing only 0.5% of global crypto liquidity, leaving substantial upside beyond the model.

- Because only 0.0045% of the world’s 360 million entities accept crypto today, leaving the $3.5T market anomaly almost entirely open.

- Because crypto has already proven demand. Regulation is opening the market. The infrastructure winner has not been decided.

We're raising to launch the first commercial version of Nostro.

Stage 1 delivers a production-ready crypto infrastructure with the first regulatory licenses and commercial validation. Stage 2 expands the architecture with the banking layer and fiat infrastructure.

This €2M round funds the platform, regulatory licensing, production infrastructure, and the first commercial customers. Every euro moves the architecture from design to real-world operation.

Our public financial model projects €3.5B cumulative profit over five years while assuming just 0.5% of global crypto liquidity. We build conservatively. We build for global scale.

The pre-round is open. The move is yours.

€1.2M

Platform, blockchain & execution.

€550K

Licensing, legal & compliance: EMI/EMD2, CASP/MiCA.

€200K

Commercial launch & validation.

€50K

Production infrastructure.